.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Financial services are undergoing one of the biggest shifts in their history, thanks to digitalization and AI.

This transformation isn’t only changing the customer expectations but also reshaping how financial institutions operate.

You don’t want to be left out?

Continue reading ⬇️

TL;DR

- Digital transformation in finance means banks and fintechs modernizing systems, adopting AI, and digitalizing processes to deliver faster, more transparent, and more personalized experiences.

- Banks are using digital tools to streamline onboarding, enhance compliance, automate back-office workflows, improve lending accuracy, personalize financial experiences, and simplify day-to-day banking.

- Digital transformation increases operational efficiency, reduces costs, strengthens risk controls, accelerates decision-making, and creates more intuitive and convenient customer experiences across channels.

- AI, automation, cloud, open banking APIs, real-time data platforms, and embedded finance infrastructure are reshaping how financial products are built, delivered, and consumed; continue reading the article for visual examples 👇

- Legacy systems, regulatory pressure, data silos, talent gaps, and organizational resistance are obstacles in digital transformation that make it challenging for institutions to modernize at scale.

- Some trends coming your way: Institutions are moving toward real-time finance, personalization at scale, embedded financial services, modular system architecture, and AI-enabled decision support.

- Digital adoption platforms, such as UserGuiding, guide users through new systems in real time, helping banks onboard employees faster, standardize complex workflows, reduce support load, and ensure customers can easily adopt digital services.

What is digital transformation in finance?

In finance, digital transformation means reshaping and modernizing financial and accounting operations with the help of technology available today.

As digitalization reshapes the financial landscape, traditional banking and financial services are undergoing a radical transformation. The shift towards digital-first solutions isn't just a trend but a revolution that's redefining how financial institutions operate, interact with customers, and manage risk."

As implied in the segment allocated to finance’s digital transformation in the iFX Expo held this year, this digitalization comes in various shapes, affecting different groups of people:

- Customers receive faster onboarding, real-time services, personalized experiences, and transparent self-service options.

- Employees obtain simplified tools, guided workflows, reduced manual work, and quicker access to data for better service and compliance.

- Management access to unified dashboards, predictive analytics, and faster insights for strategic decision-making and performance tracking.

- Regulators and partners benefit from improved transparency, standardized data sharing, and automated compliance reporting.

Now, let’s dig up the areas where this change takes place one by one 👇

What are the use cases of digital transformation in finance?

Digital onboarding & KYC

From the customers' perspective, digital transformation starts with the ability to handle financial matters that require them to go to a bank or service provider through a mobile phone.

For example, customers can verify their identity through e-KYC while registering on a mobile banking application for the first time or setting up a new device to access their bank account digitally.

These applications often provide customers and internal users with guided onboarding flows for them to successfully explore the platform and achieve their goals without confusion.

Doing so is crucial because 48% of global banks declare that they lose clients due to slow and inefficient onboarding.

So, let’s check how HSBC UK overcomes this challenge and onboards their customers to their mobile application:

With video/biometric identity checks (like HSBC does ☝️), customers don’t have to wait for a Telephone Security Number or follow a more complex and manual procedure since this process eliminates the need for visiting a bank and enables customers to enjoy the perks of digital banking, such as automated credit and loan decisioning.

⚠️ Mobile banking applications also offer fraud detection during onboarding to prevent fake accounts, identity theft, and unauthorized access.

Core banking modernization and core system migration

Core banking modernization means upgrading the old banking systems that handle accounts, payments, and transactions.

Instead of relying on decades-old mainframes, banks move to modular, cloud-based platforms that are faster, easier to update, and can connect with modern apps.

This shift helps banks in several ways:

- faster decision-making through real-time data and automation, reducing approval times for loans or transactions.

- higher customer satisfaction from quicker, more intuitive digital experiences.

- lower operational costs by replacing manual tasks with automated workflows.

- greater agility to launch or update financial products without lengthy development cycles.

How do I know? 👇

Ernst & Young’s analysis shows 20-35% gain in operational efficiency, primarily through real‑time processing after their alliance with FIS; the same analysis also suggest that systems’ maintenance costs got significantly lower.

A study by IBM reports 49% improvement in client experience through cloud-native modernization and 46% more efficient data access thanks to faster retrieval and processing via cloud-native analytics.

🌟 In addition to these, there is also a real-life example from Oracle Cloud, which helped a global bank, Houlihan Lokey, double its revenue in five years through the automation of core accounting processes and faster reporting.

Everywhere we turn, automation is allowing us to manage a much larger organization at a cost that is not changing." - Allen Fazio, Chief Information Officer @Houlihan Lokey

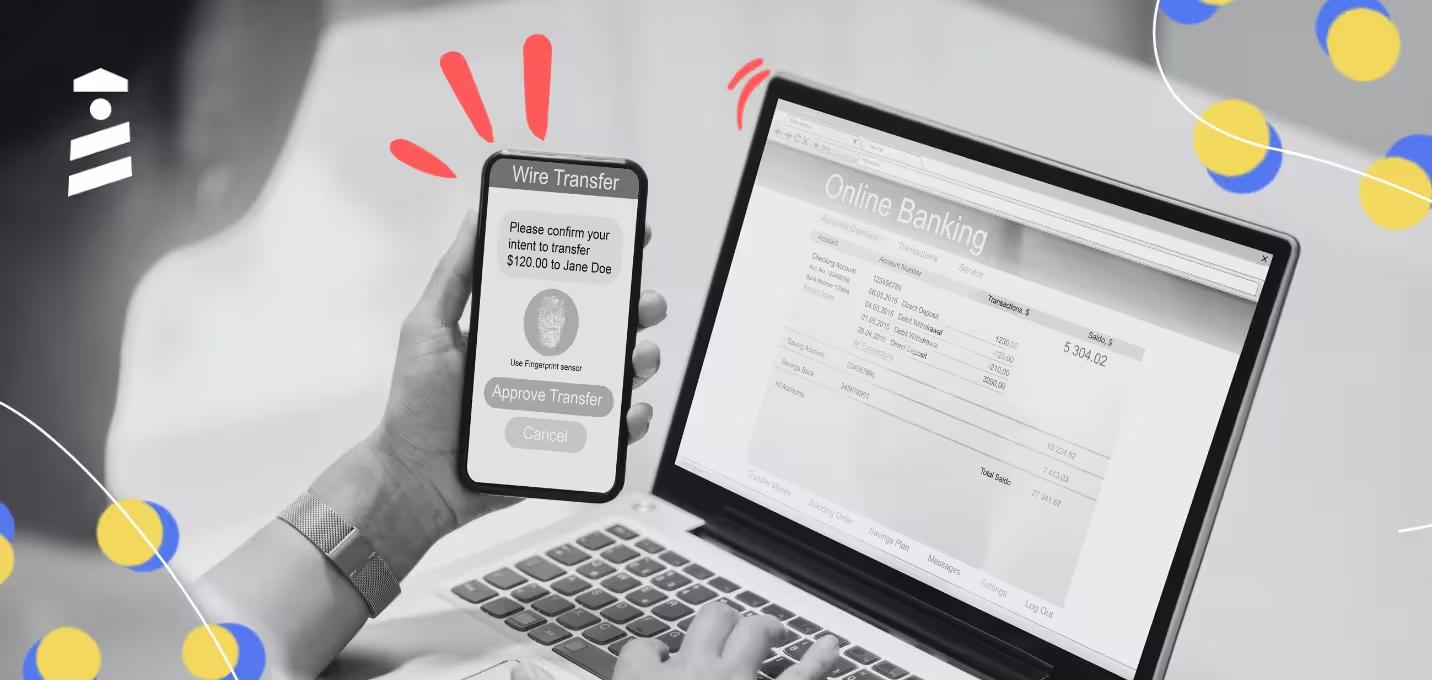

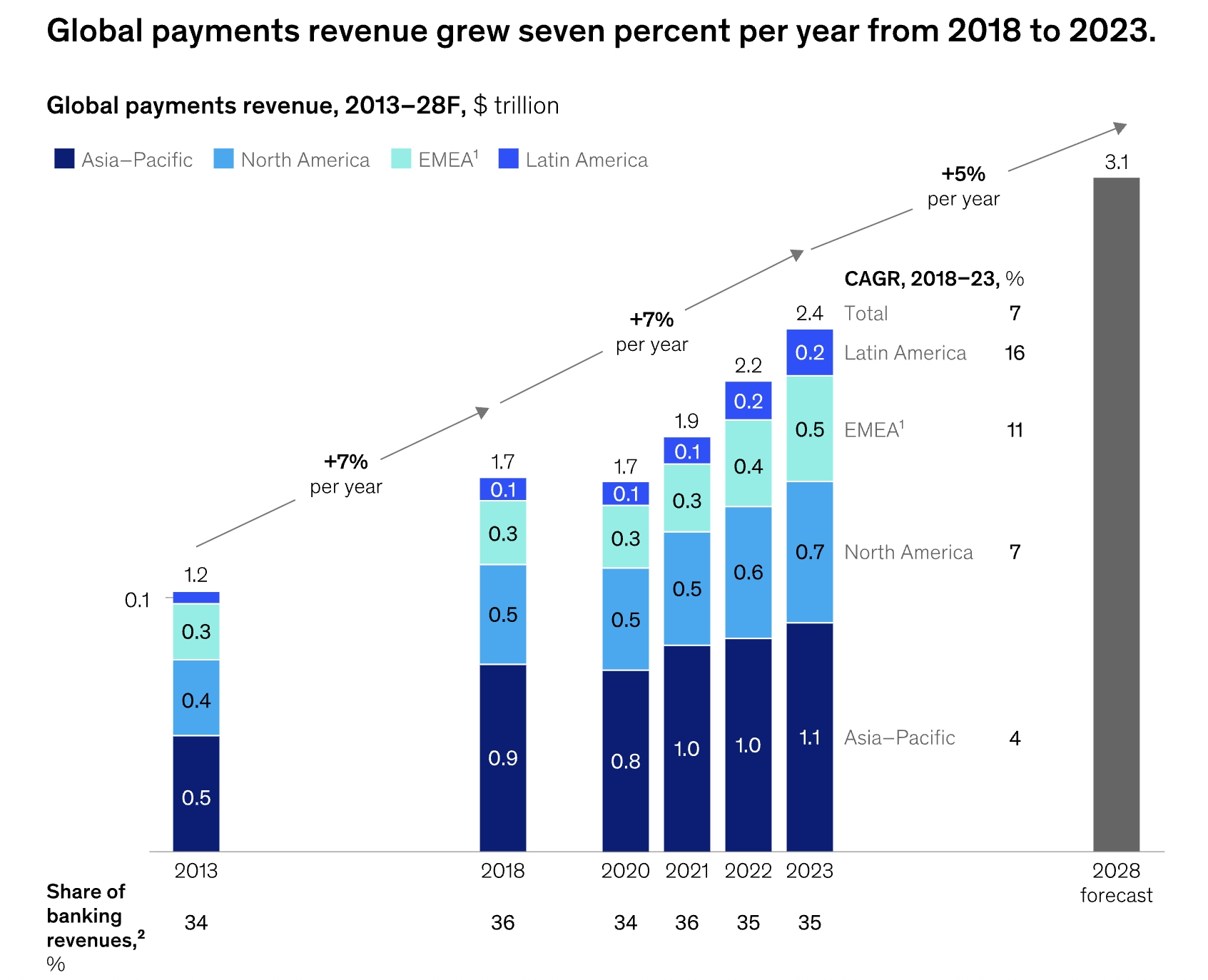

Payments & transaction processing optimization

Instant payment, real-time clearing, and cross-border payment processes are the heart of online banking, as many customers prefer to process their payments in real time, transfer money, pay bills, and complete a purchase instantly no matter where they are.

Some hard facts here:

1️⃣ According to McKinsey & Company, the global payments industry grew 7% annually from 2018 to 2023 and is projected to grow 5% annually through 2028, adding $700 billion in revenue to reach $3.1 trillion, making up 35% of global banking revenue.

2️⃣ A whitepaper by Mastercard projects that “the value of transactions processed using real-time payments technology” is expected to grow by 289% between 2023 and 2030.

These two statistics are among the reasons banks need to meet growing customer expectations by moving toward faster and more transparent payment systems that allow customers to move money within seconds instead of days.

Samarth Bansal, General Manager of Wise, says that Wise increased the percentage of transactions processed in under 20 seconds from 61% to 65% in the past year to remove the bottlenecks in global payment flows.

Currently, 62% of all payments on our network arrive instantly. When we say "instant," we mean that the payment lands in the recipient's account in under 20 seconds." - Roisin Levine, Head of UK and Europe Partnerships @Wise

That being said, optimized transaction systems also reduce errors, delays, and failed payments, giving customers a smoother experience whether they’re sending money abroad, paying a merchant, or using a mobile wallet.

💡 Mobile-friendliness, fraud detection and prevention, local acquiring, automations, contactless payment, and unified commerce are all steps that banks need to take in order to optimize the payment process.

Risk, fraud detection, and compliance automation

Risk and compliance automation saves banks significant time and reduces error rates.

👉 For customers, this transformation means safer transactions and fewer false alarms through transparent and compliant systems that handle data responsibly and follow regulations.

How can banks use technology to identify, prevent, and respond to risks and fraud while staying compliant with financial regulations?

- AI and machine learning (ML) models that monitor transactions and detect suspicious or abnormal activity in real time; for example, in 2023, Visa was able to block $40 billion worth of fraudulent transactions thanks to AI.

- Automated compliance and reporting systems that handle regulatory submissions, audits, and documentation; Scotiabank, for instance, experienced a 75% reduction in report generation time and 70% fewer data errors after implementing regulatory reporting automation.

- Centralized risk management tools that bring credit, market, and liquidity risks together into one view, helping banks react faster to potential threats, just like SeABank, which gained a 360° view of operations after implementing Oracle’s risk and finance solution.

Loans, credit underwriting, and decisioning

Traditionally, loan approval and credit evaluation rely on manual reviews of financial statements, credit scores, and collateral documents.

Thanks to digital transformation, this slow, error-prone, and often inconsistent process turns lending into a faster and more efficient process through data and automation, such as:

👉 Automated credit scoring powered by AI and machine learning to assess risk more accurately.

👉 Digital underwriting systems that analyze hundreds of data points in seconds (income, spending patterns, payment history).

👉 Predictive models to personalize loan offers and interest rates based on customer behavior and repayment likelihood.

All of these result in faster loan decisions, lower default risk, and improved financial inclusion (serving people who might lack traditional credit histories); don’t believe me?

Check these statistics out:

A research paper found that algorithmic underwriting produced 10.2% higher loan profits and 6.8% lower default rates compared to traditional underwriting; in addition, Fora Financial experienced an over 50% reduction in bank statement verifications, eliminating unnecessary verification requirements and lowering early credit losses by automating data extraction from loan origination documents.

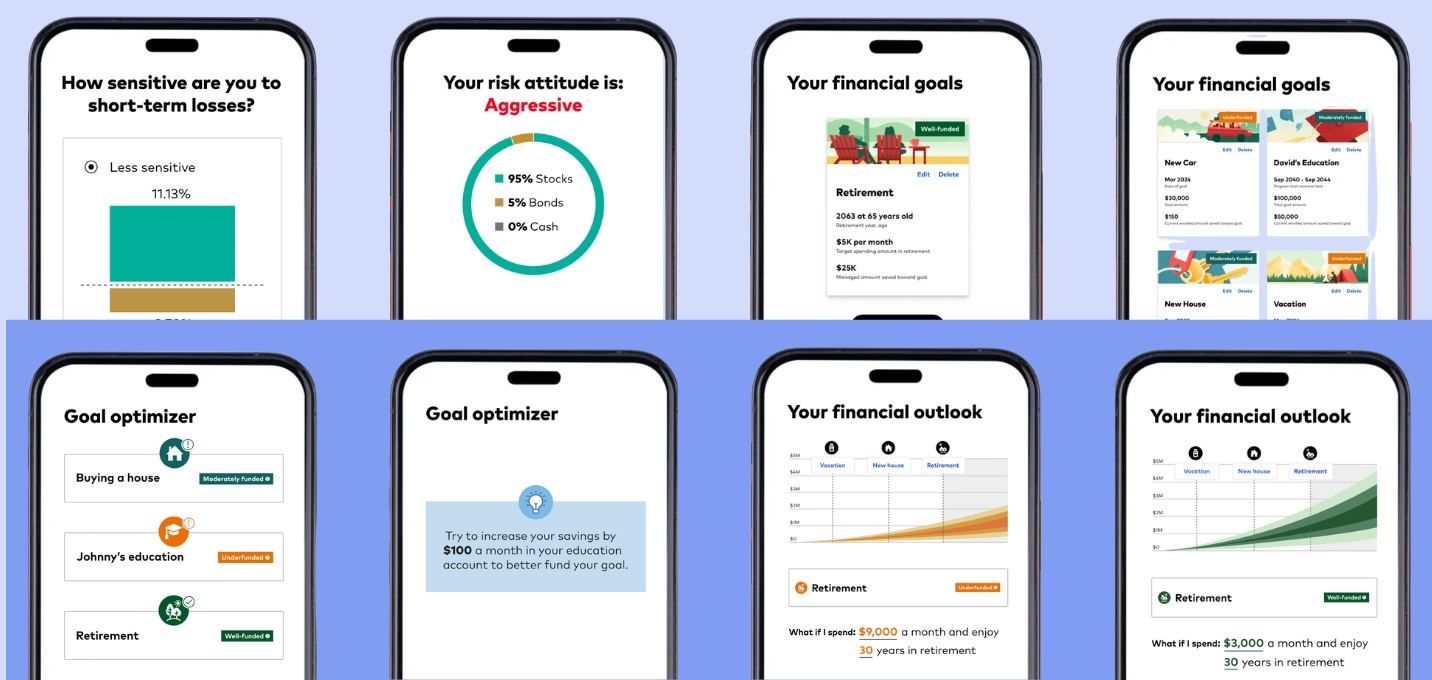

Wealth/portfolio advisory, robo-advisors

Wealth and portfolio advisory is an exclusive process when handled by human advisors, requiring manual portfolio construction, in-person meetings (or mailed statements), and long approval cycles.

However, the automation of portfolio generation, robo-advisors/advice engines, and scenario modeling and forecasting accelerates this process significantly.

Digitalization in this context helps both financial institutions and customers:

👉 The former gets to serve thousands of clients with personalized advice automatically with fewer errors (and no human bias) in portfolios, cutting costs via automation and increasing customer retention through consistent and data-based recommendations.

👉 The latter gets to access personalized investment advice that showcases faster and transparent decisions 24/7 through apps and online dashboards, yet still pays less compared to traditional human-only advisory models.

What’s even better, financial advisors are on board with this change: 40% of financial advisors wish to implement an AI to understand what they should do to meet customer expectations and increase satisfaction.

💡 That’s why the robo-advice assets were expected to surpass $1.2 trillion at the end of 2024 after hitting a milestone of $1.089 trillion in 2023.

Customer experience, digital channels, and omni-banking

Before digital transformation, customers interacted with banks mainly through branches or call centers.

Every channel worked in isolation: You couldn’t start a process online and finish it in-app or in-branch.

With omni-banking, customers can:

- open an account online, sign documents on mobile, and get instant support through chat through a single medium.

- retrieve personalized insights, reminders, and recommendations, such as spending alerts, savings tips, or credit-limit offers that banks use data and AI to send.

- get assistance from digital assistants and chatbots to handle routine queries 24/7, eliminating the need for human support even in complex cases.

In short, omni-banking ensures that customers have a seamless and personalized experience no matter when, where, or how they interact with their bank.

This matters, because 91% of consumers are more likely to shop with brands that recognize, remember, and offer relevant recommendations, according to Accenture’s Personalization Pulse Check Report.

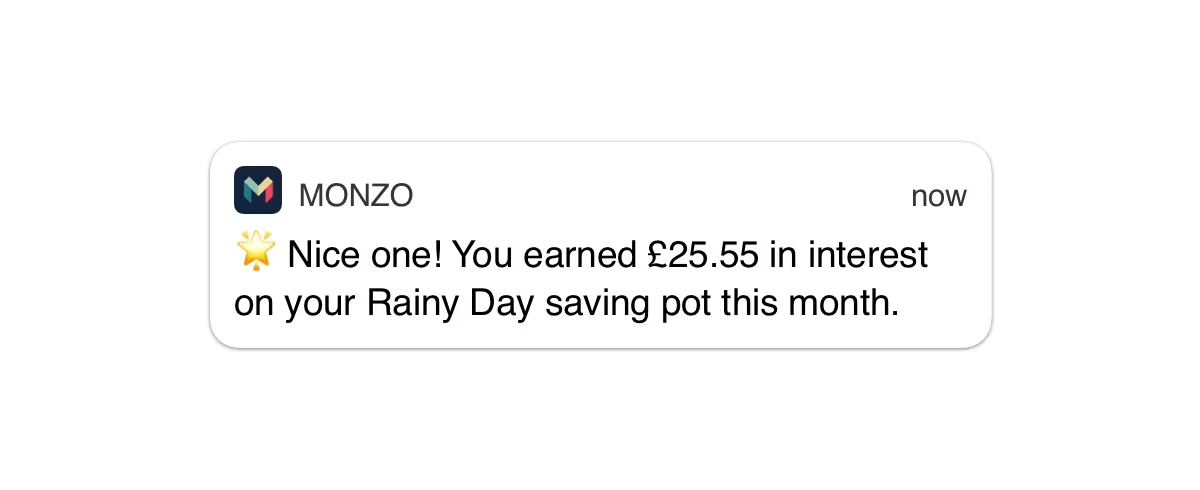

Repeating what I said above, these push notifications vary in type; for example, HSBC sends you instant notifications regarding transactions if you allow them:

If you do so, you’ll receive instant notifications on your phone when you send or receive money, transfer between accounts, make branch and ATM transactions, and purchase items such as memberships, subscriptions, and shopping through your direct debits and card.

But once banks start to bring personalization into it, these types of notifications come about:

Back-office efficiency and process automation

Besides the customer-facing aspects of finance, such as digital onboarding, omni-banking, and robo-advisors, there is an aspect that turns the wheels behind the scenes.

I’m talking about repetitive and rule-based administrative work, including but not limited to account reconciliation, data entry, reporting, and approvals.

With the arrival of digital transformation, these tasks can be automated thanks to technologies like Robotic Process Automation (RPA) and workflow engines.

Automation also supports Straight-Through Processing (STP), meaning transactions move automatically from initiation to settlement without manual intervention.

Thanks to the technology used in speeding up these processes:

👉 Banks can cut operational costs and processing time; thus, customers no longer have to wait for days for loan approvals, transfers, or account updates.

👉 Banks reduce human error and compliance risk while customers process transactions accurately, reducing delays and corrections.

👉 Banks are able to free employees to focus on higher-value tasks like customer service or strategy, and customers get to benefit from better rates and reduced fees.

💡 Let’s elaborate on this shift with examples: JPMorgan Chase’s COiN (COntract INtelligence) platform saved 360,000 hours of manual work annually through automating document review and contract analysis.

Along with JPMorgan Chase, Danske Bank used RPA to automate reconciliations and cut the process time by 80% (equivalent of 300 full-time employees worth of work).

Data, analytics, decision support, and finance transformation (FP&A, forecasting)

Now that financial institutions have stepped fully into the world of technology and are surrounded by data, the next step is to turn that data into smarter financial decisions through real-time dashboards, predictive analytics, and scenario planning.

Let’s see why these items are a part of the digital transformation in finance:

FP&A (Financial Planning & Analysis) systems help banks and institutions forecast performance, assess risk, and make better investment or lending decisions.

With embedded analytics, insights are built directly into day-to-day tools; for example, a risk manager or branch executive can see real-time profitability metrics inside their dashboard without extra reports.

Curious what a FP&A dashboard looks like? Let’s check one of the most well-known software programs in finance teams, Anaplan:

As customers get to benefit from a more stable and transparent banking system (due to data-driven insights that reduce risk and errors in lending and investments) with personalized services (thanks to predictive analytics, which allow banks to tailor offers, interest rates, or financial advice to individual needs), it’s a win-win for both sides.

💡 According to Oracle, an anonymous major credit union in North America with more than 150 unaligned source systems used their financial solution as their central data repository and improved forecasting accuracy and regulatory compliance.

Embedded finance/open banking & API ecosystems

First, let’s get more accustomed to these two terms:

Embedded finance allows banking services to appear inside non-bank platforms.

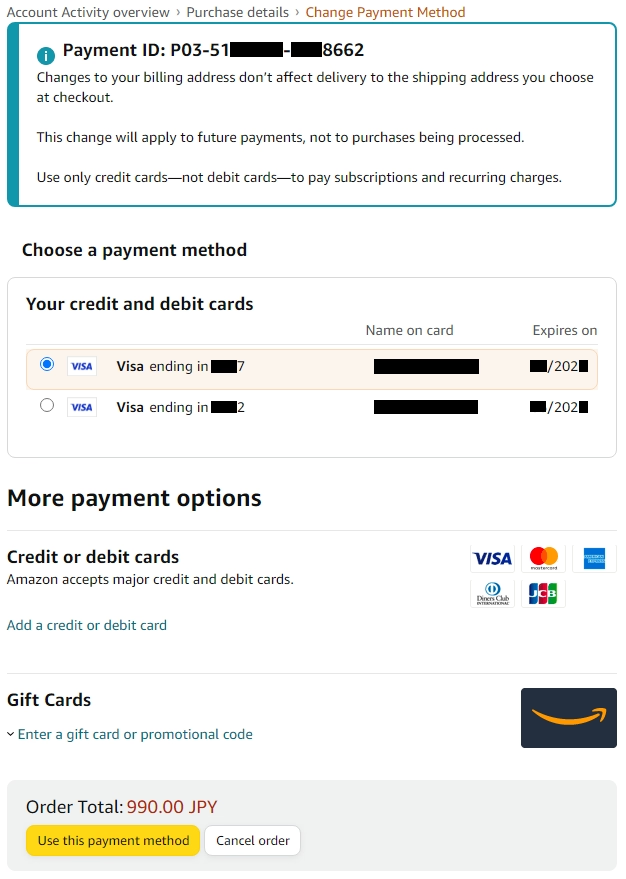

For example, when you shop through an e-commerce application, you pay within the same platform and not through your bank’s website.

Remember the last time you ordered something from Amazon? You didn’t need to visit your bank or use a banking application because you could pay with one click through your stored cards, credit options, or digital wallet.

💡 Payments currently make up about 44.2% of the embedded finance market share as of 2024.

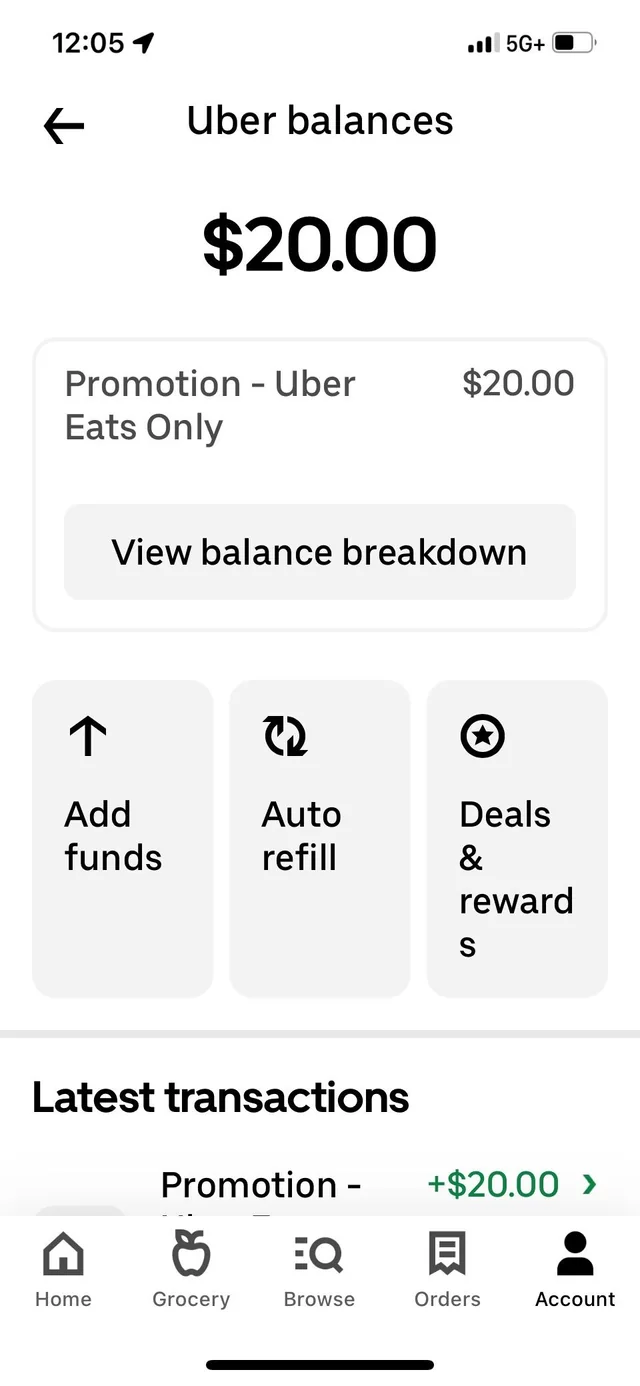

Likewise, think about how your favorite ride-sharing app works; it offers financing directly inside its dashboards.

Let’s take Uber in hand and review its payment process:

Uber Cash is a system for users to add funds to their Uber balance, which can be used to pay for rides and food orders, all powered by banking partners behind the scenes.

Moving onto the second term, open banking uses APIs (application programming interfaces) to securely share customer data between banks and third-party providers.

Now, let me tell you what this shift has brought to the table:

- Along with enabling partnerships with fintechs and retailers, embedded finance has conveniently helped customers to pay for a service/purchase an item with one click.

- It also expands reach beyond traditional banking channels, growing from $148.38 billion in 2025 to $1,732.53 billion by 2034, according to a forecast estimation.

- APIs generate new revenue streams through integrated financial products and also improve service availability, average response time, error rates, and call success, suggest Starling Bank, compared to industry competitors.

What are the benefits of digital transformation in finance?

Now that you know what has been going on in the finance world, let me introduce you to the benefits of these technological changes!

🏦 For banks and financial institutions, digital transformation has:

- improved efficiency, cut costs, and scaled operations through streamlining manual tasks like reconciliation, reporting, and compliance reviews using automation and cloud systems.

💡 Take M&G Investment UK for example; they used Oracle Cloud EPM to enhance scenario planning and reduce manual work, and achieved faster reporting and better forecasting accuracy.

- strengthened risk management and enabled data-driven decisions by the integration of analytics and AI.

💡 This benefit is quite important since 22% of financial leaders cite fragmented security, risk, and compliance as a major barrier to success.

- increased agility and ensured compliance through cloud platforms that adjust banks quickly to new regulations and market volatility while maintaining transparency and audit readiness.

💡 This is exactly what ended up happening to Deutsche Bank after their partnership with Google Distributed Cloud: Not only did they see a reduction in server counts and reduced costs by 25%, but also improved workload density by 70%.

- created new revenue streams and helped banks stay competitive thanks to fintech partnerships, embedded finance, and subscription-based offerings.

💡 Reminder: Most of the embedded finance activity (about 62% of the total market in 2024) came from the consumer (B2C) segment; that says a lot about how effective they are.

👥 Digitalization in finance has helped customers to:

- receive a faster, more reliable, and transparent service with automation accelerating payments, loans, and updates while reducing human error, leading to quicker approvals and fewer disruptions.

💡 From the customers’ side, real-time payments are significant as middle-market companies say 77% of customers think so.

- gain personalized and convenient experiences that allow them to access tailored financial products anytime, across any channel, with consistent UX and proactive support.

💡 Personalization is an area that must be covered by every bank because 72% of consumers say personalization influences where they bank; on top of this, 74% of consumers across generations express a desire for more personalized banking services.

- feel safer when managing their finances online thanks to AI-powered fraud detection, real-time alerts, and transparent data sharing.

💡 70% of consumers are on board with using AI for advanced fraud detection!

Some examples of technology driving finance transformation:

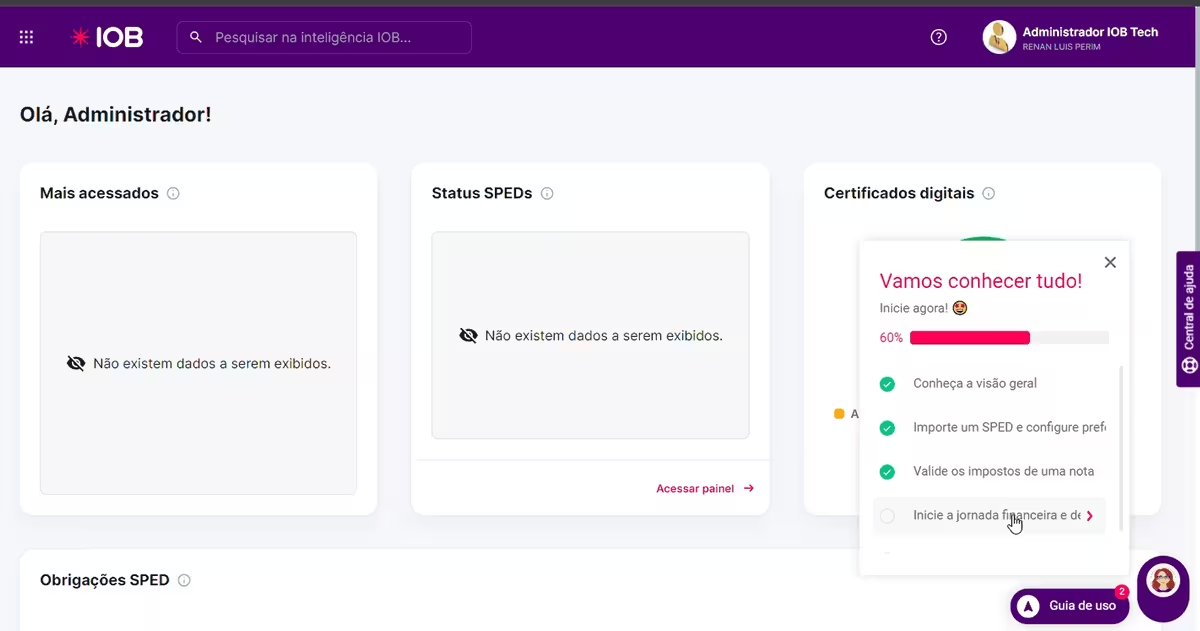

1- Web app onboarding example #1: Grupo IOB

Accounting management solution, Grupo IOB offers an onboarding checklist for users who have just landed on the platform, involving four key items for them to complete:

What’s even better, the platform also involves an interactive guide that walks users through key features of the platform to ensure the onboarding process moves smoothly 👇

Besides checklists and guides, Grupo IOB benefits from surveys, announcement modals, and hotspots to offer a complete digital onboarding experience to users; as a result, they saw a huge boost in the completion rate of their initial onboarding guide (up to 75%).

However, this isn’t the only positive outcome: They also stated a significant reduction in support calls since they started offering an interactive guide with each necessary element included.

🤭 Psst, Grupo IOB used UserGuiding for all the mentioned user experience elements above.

What makes this a good example of digital transformation?

✔️ The onboarding checklist offers users a structured path they should follow to explore and make the best of the platform.

✔️ The interactive guide helps new users get to the aha! moment quicker as it walks them through the key features of the platform, aka the solution they are looking for.

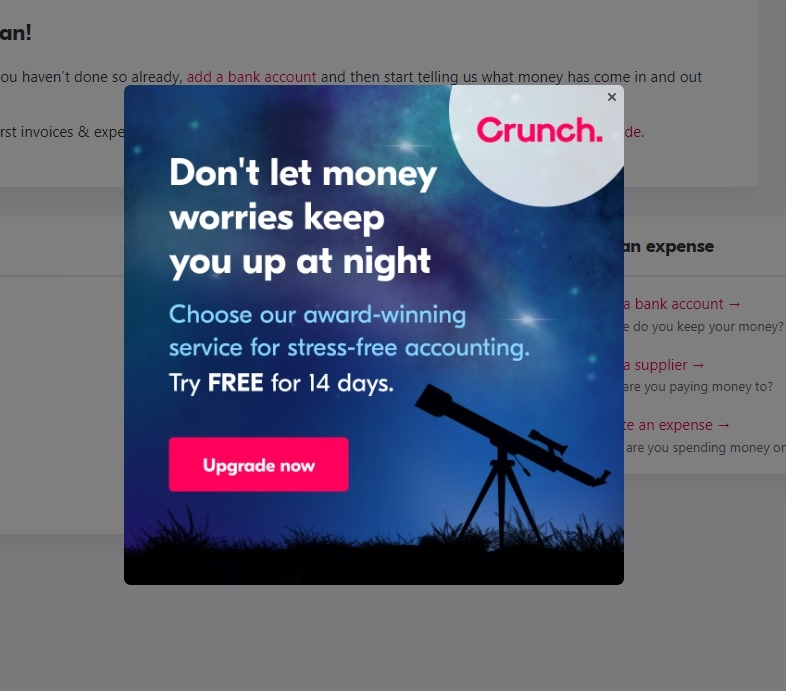

2- Web app onboarding example #2: Crunch

Crunch, an accountancy software, was trying to find a way to increase the conversions and engagement rate of freemium users.

What they chose to apply to their users’ experience was announcement modals 👇

This modal not only increased the number of add-ons and upgrades but also improved the engagement rate altogether.

Once again, this modal was made with UserGuiding 🌟

What makes this a good example of digital transformation?

✔️ The announcement modal is to the point and encourages users to take action through personalized reminders.

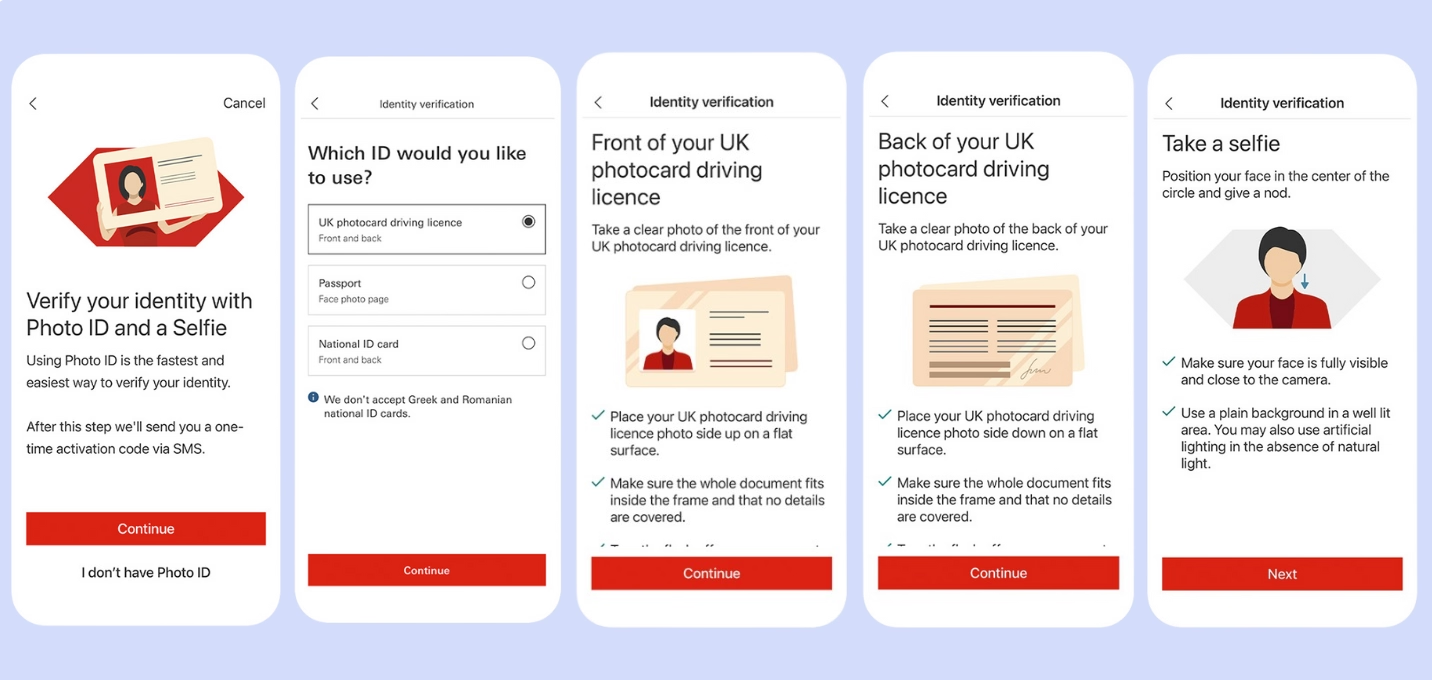

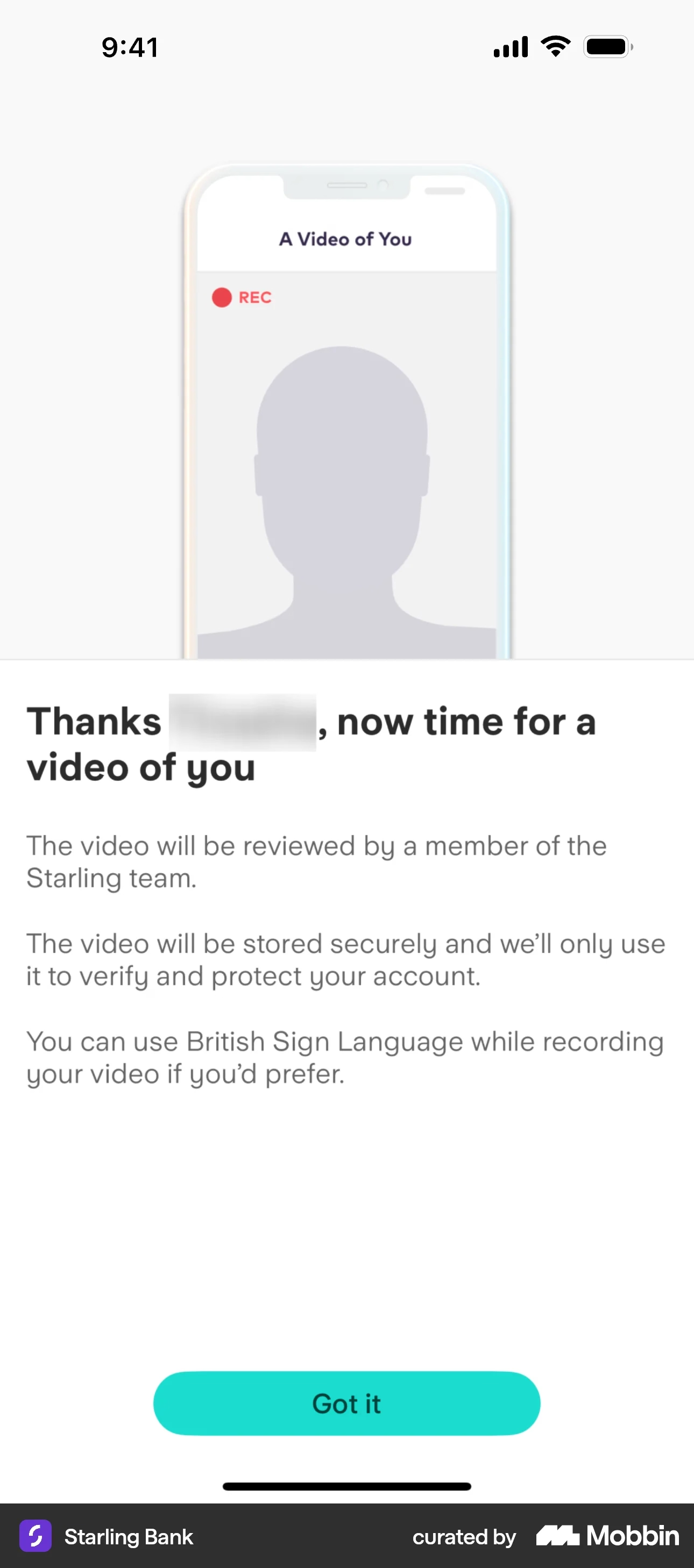

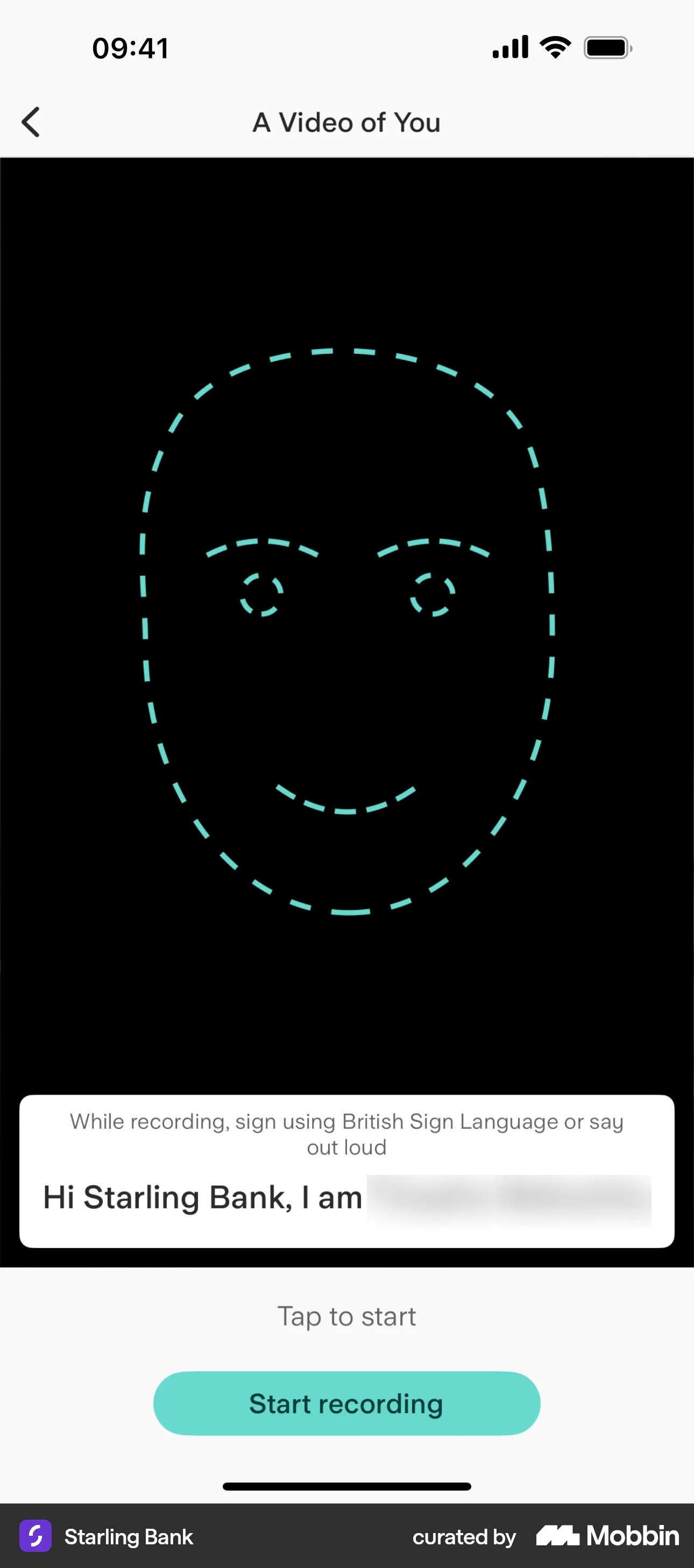

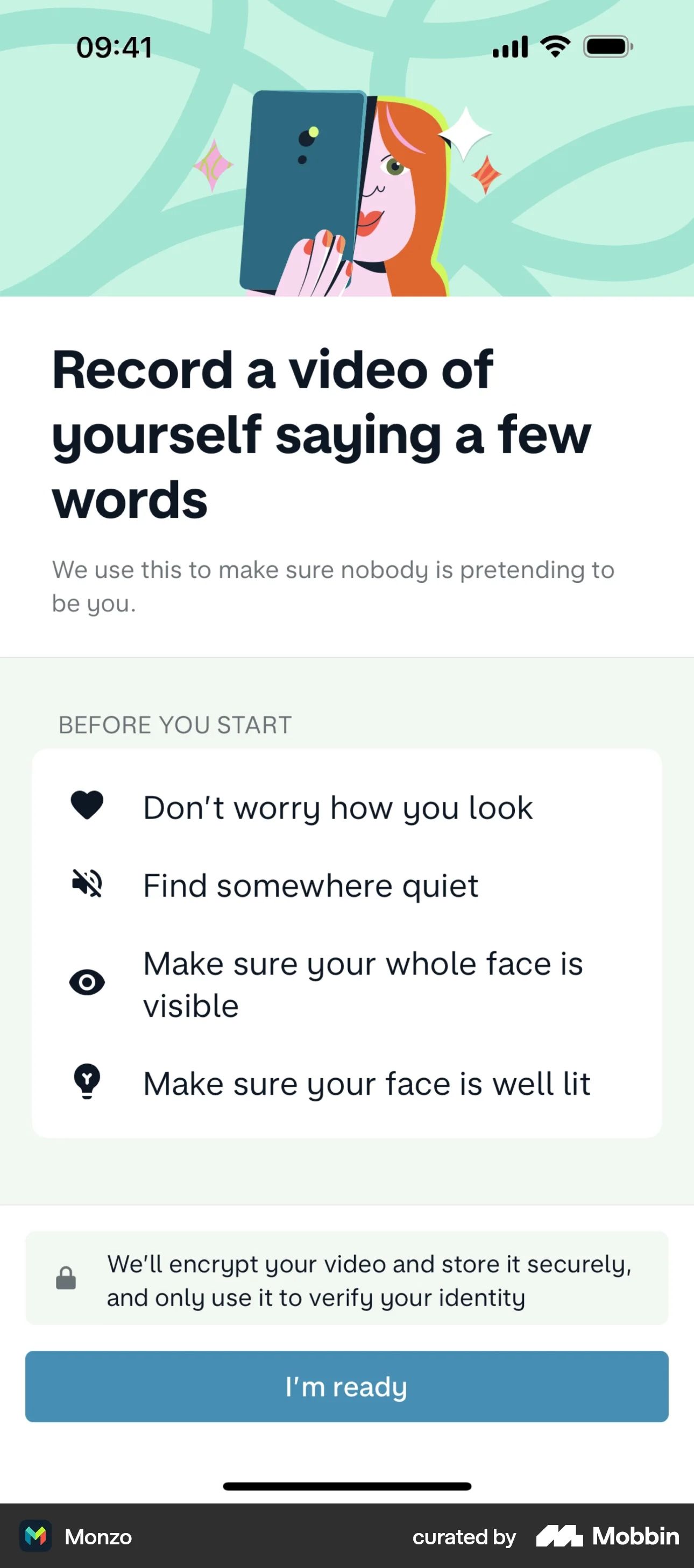

3- Mobile banking app onboarding and KYC example #1: Starling Bank

As a mobile-only bank, Starling Bank itself is a great example of digital transformation in finance.

First, the application involves a top-notch set-up process; what differentiates it from the others?

During the KYC sequence (confirming the identity of the customer), it asks the general questions we are all very familiar with, such as number and ID verification.

Then, it requests a video to be taken by the customer so that a dedicated team from Starling can review it to ensure it’s the correct person (and not a fraud):

Starling Bank’s mobile verification method: face recognition.

Then, the customer takes a video, says the phrase below the screen part, and stops recording to upload the video.

What’s more, it offers a product tour to show users around the application:

As the application got a brand-new home screen, Starling Bank started offering a short product tour to existing users for them to understand where they can find the sections/buttons that got relocated within the app.

Alternatively, this product tour serves as a welcome tour for new users who just got landed into the application.

What makes this a good example of digital transformation?

✔️ The KYC process is loaded, requiring a number, personal information, ID verification, and a video verification, but it significantly decreases the risk of account takeovers and fraud.

✔️ The product tour shows users around, helping them get to know the application and encouraging them to explore freely.

✔️ It isn’t a mandatory tour; it doesn’t interrupt any users’ flow, instead, it’s there to guide them if they need any help.

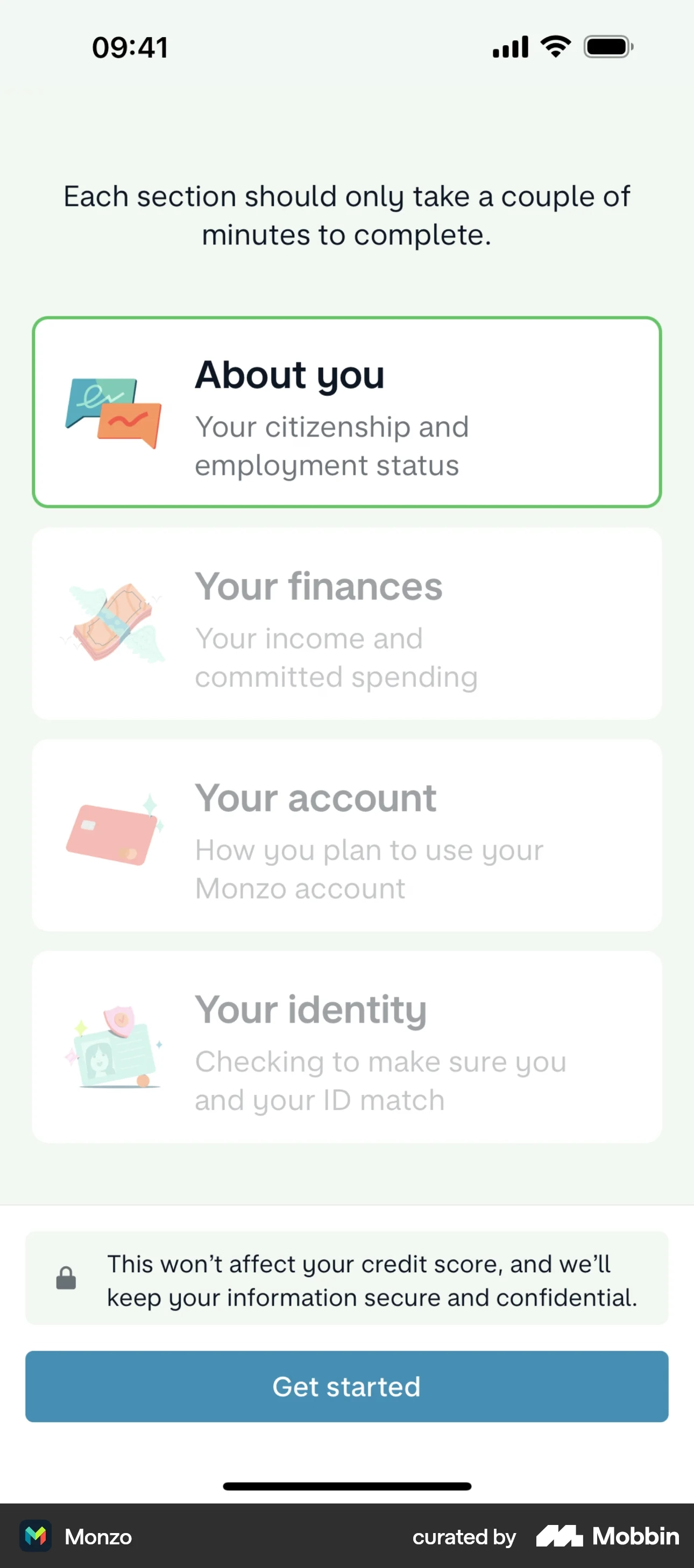

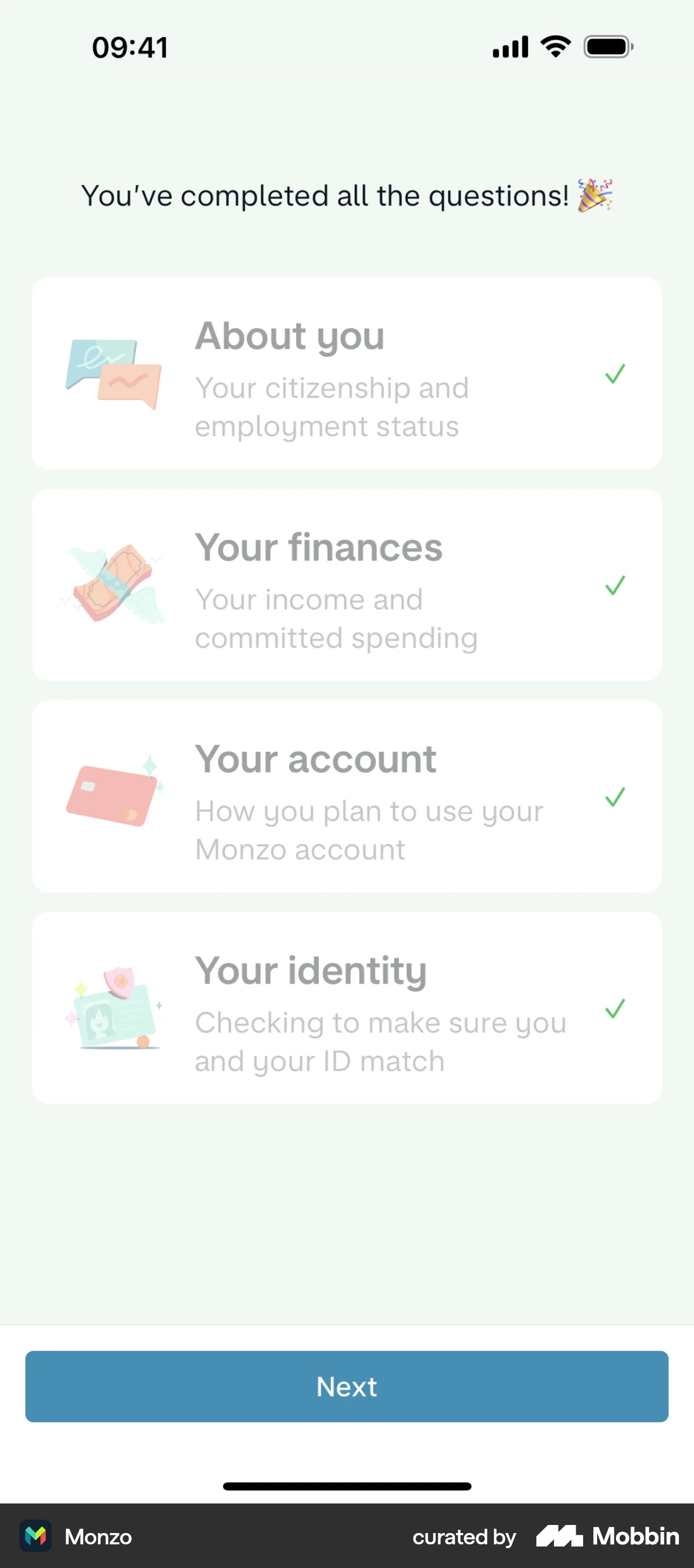

4- Mobile banking app onboarding example #2: Monzo

Monzo, another mobile banking application, also offers onboarding elements in order to accelerate the onboarding process (along with filling the required blanks), such as an onboarding checklist:

Monzo’s onboarding checklist asks users to complete four different sections: information, finance, account, and identity.

After users move on to the last section, the KYC process will begin and ask users to verify their identity through ID (or other options like a driving license and a passport) and video:

When users answer these questions, the application congratulates them and allows them to reach all features:

What makes this a good example of digital transformation?

✔️ With four short sections, the onboarding checklist allows users to move forward through the KYC process on their own pace; the checklist is also a great choice because users can always go back to it and check their progress or where they left off.

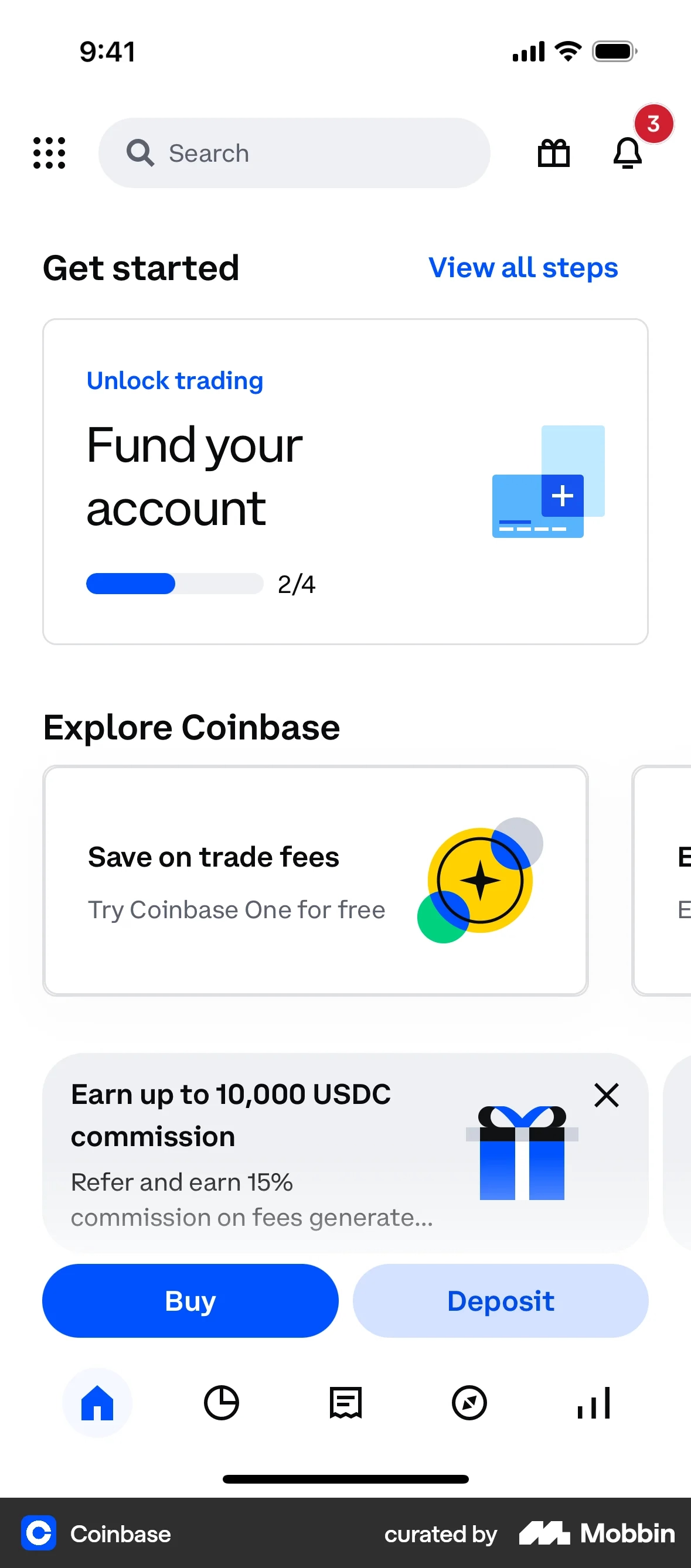

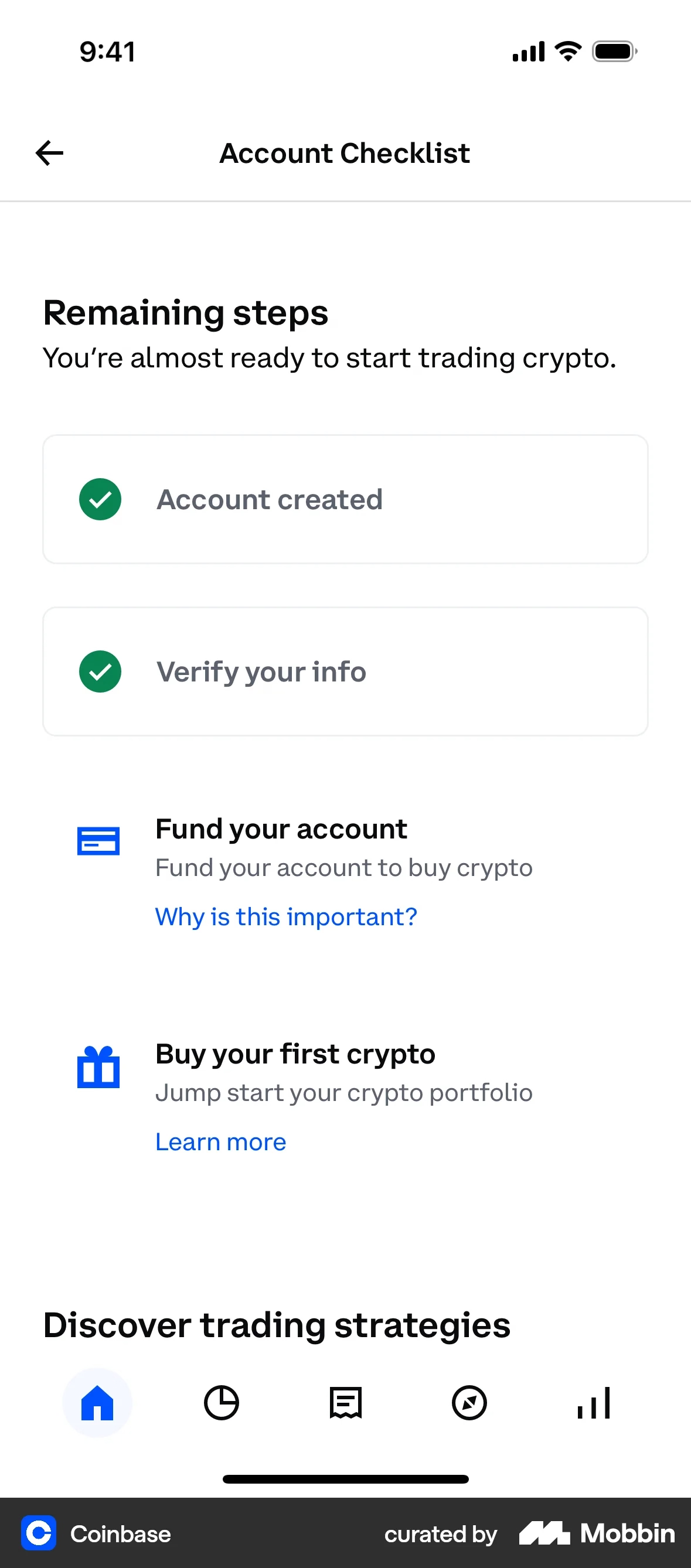

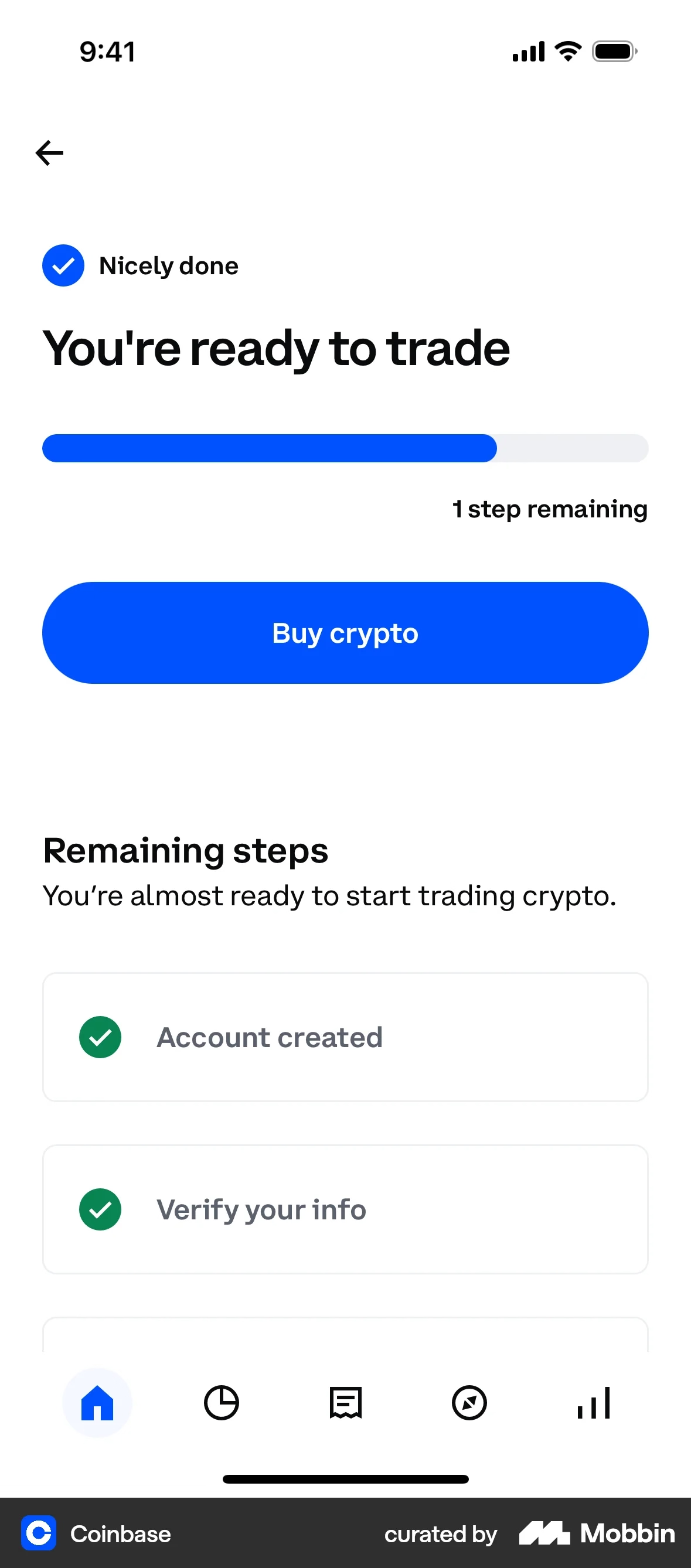

5- Mobile finance app onboarding example #1: Coinbase

A cryptocurrency platform, Coinbase, includes a great example of onboarding with a get started section 👇

When users click on it, they face with a checklist of four short items that will help them use the application to its full potential:

The items that users need to complete to finish setting up their account are as follows:

- create an account,

- verify information,

- fund account,

- buy crypto.

A progress bar is also located right above the checklist so that users can easily follow their progress and continue by simply clicking on a button to move to the next step.

What makes this a good example of digital transformation?

✔️ The account checklist has four simple items and the copy is just as short, not losing users due to complex instructions with a big cluster of to-dos.

✔️ The progress bar encourages users to continue since it shows them how far they’ve come.

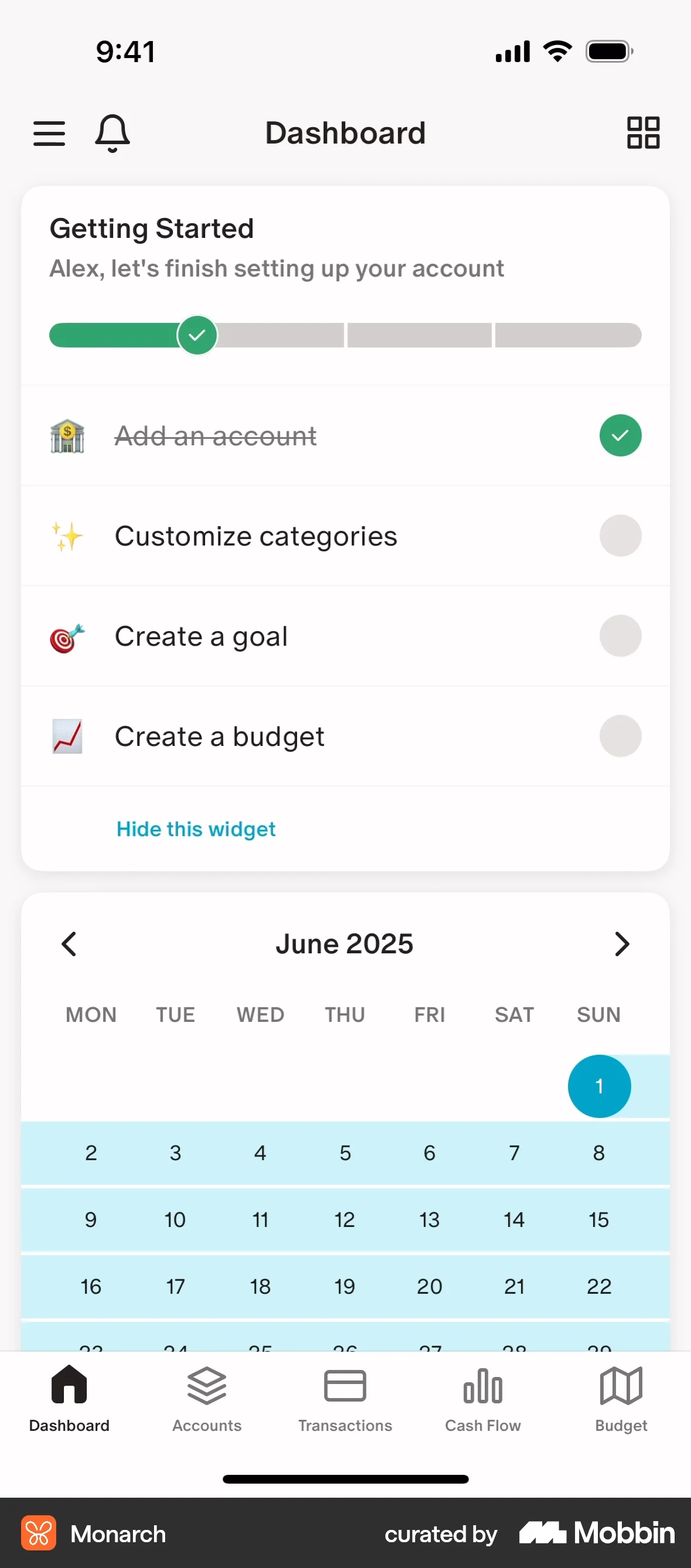

6- Mobile finance app onboarding example #2: Monarch

As a finance application, Monarch has an intuitive interface for users to plan and track their budget; what’s really plausible is the checklist that helps users set up their account:

Monarch’s onboarding checklist appears as a widget at the top of the dashboard screen; it involves four items that need to be completed: adding an account, customizing categories, creating a goal, and creating a budget.

Besides placement, the checklist widget comes with a progress bar for users to check their progress, which they can hide as a whole if they wish.

What makes this a good example of digital transformation?

✔️ The onboarding checklist is placed correctly (on the top of the dashboard) and each item is short enough to grasp quickly; plus, the checklist is supported with emojis.

✔️ The widget also involves a progress bar for visualization, and the whole set of widgets can be hidden.

7- Traditional bank digitalization example: DBS

The largest bank in Singapore, DBS, focused on three pillars of digitalization:

- Digitizing to the core: They repurposed their technology stack to run on cloud and open source to be an AI-powered bank; now, more than 60% of small to medium businesses begin their relationship with DBS digitally.

- Thinking of the customer journey: Their mobile-only bank, Digibank allows you to become customer under 90 seconds; moreover, the application uses AI-driven virtual assistants only with a 80% successful answer rate.

- Adopting a start-up culture: Investing in a start-up mindset, the bank welcomed a high pace workflow while being open to innovation, which enabled them to experiment over 1,000 projects and earned them more than 50 industry partners.

This is how the former Chief Information Officer of DBS, David Gledhill, elaborates on the Digibank example:

The outcomes of our transformation are speed to market, scalability, experimentation, and all of those things that you see in these technology companies. One successful example would be a bank offering we did in India. We were trying to figure out how to scale our presence in India, where we had very few branches. So how do you attack a market of a billion people? We came up with a mobile-only offering.

Now first of all, we had no clue how it was going to work. I understand how to create a mortgage product and sell it, and I know how to build systems for it. But how do you build a mobile-only bank in India and attract customers at scale? No idea.

So, we had to learn as we go, which means we had to iterate very fast. We were actually pushing out releases weekly into the app store.”

What makes this a good example of digital transformation?

✔️ They leveraged APIs and microservices in order to grow their in-house tech capabilities, and they succeeded at laying the foundations to become an AI-powered bank.

✔️ With virtual assistants, they offered assistance to their customers and were able to offer a mobile-first approach.

8- Digital onboarding example: HSBC

Upon hearing customer complaints on opening a new business account, HSBC US decided to simplify and digitize their onboarding process.

How did they do so? 👇

They created a digital platform and digitalized the whole onboarding process for both domestic and international businesses, which allowed them to onboard in three days or less.

💡 This digitalization process was rated excellent by 82% of their customers.

On top of that, the digitalization of the information and transaction portal allows customers to benefit from:

- accessing a global cash management solution,

- managing liquidity,

- making and stopping payments,

- viewing account balances,

- and transferring funds around the world.

For visualization, let’s take a look at the liquidity management dashboard:

What makes this a good example of digital transformation?

✔️ This digital onboarding example took face-to-face onboarding from a complicated, time-consuming, and worst, a paper-intensive process to a digital process where customers can open business accounts a lot faster all around the world with the help of simplified and digitized components.

9- AI for productivity example #1: Citi Bank

This year, Citi launched a suite of AI tools to simplify workflows and help employees increase their productivity.

For example, their document intelligence tool, Citi Stylus shortens the time spent on an article by providing insights from documents in various formats along with summary and comparison sections.

Citi Assist, on the other hand, can search through Citi documents regarding policies and procedures to minimize risk and ensure compliance.

By improving internal efficiency, Citi believes that the client experience will also rocket

Citi believes that increasing internal efficiency and enhancing client experience go hand in hand, and these tools act as the bridge between the two.

What makes this a good example of digital transformation?

✔️ The usage of AI in finance workflows will not only increase productivity between employees but also help them understand customers more effectively and deliver personalized interactions.

10- AI for productivity example #2: HSBC

Just like Citi, HSBC also implements AI to increase employee efficiency in over 600 use cases, including:

- Developer efficiency: 20,000+ developers use AI coding assistants, reducing coding time by 15% and improving feature delivery speed and safety.

- Operational productivity: Generative AI assists service teams handling 3M+ client interactions annually, cutting turnaround times and improving customer experience (with 88% rating HSBC easy to deal with).

- Customer support acceleration: AI-generated call and chat summaries help agents resolve requests faster with shorter wait times.

- Credit process automation: AI supports credit analysis write-ups using internal and external data, reducing time to complete credit applications.

- Financial crime detection: AI models identify 2–4x more suspicious activity with significantly higher precision.

- Daily workflow enablement: Employees across teams use LLM-based tools for translation, document analysis, and writing assistance to complete tasks faster and more accurately.

What makes this a good example of digital transformation?

✔️ The usage of AI positively affects internal teams along with clients, helping one party to speed up and automate manual work, while ensuring that the other one receives better experiences.

Obstacles in digital transformation in finance

You might ask yourself what is keeping the finance industry away from digital transformation; let me quench your curiosity in three parts:

Technology and infrastructure barriers:

- legacy systems and interoperability,

- technical debt and data silos,

- vendor lock-in

Let’s focus on what technology and infrastructure barriers involve one by one:

Block #1: Many financial institutions rely on decades-old core systems that weren’t designed to connect with modern digital tools or cloud services. Although these legacy platforms hold valuable data, they struggle to share it efficiently across departments or with newer applications

👉 The Core Banking Without Compromise report supports this, revealing that 55% of banks identified outdated core solutions as the biggest obstacle to achieving their business goals.

Block #2: PwC highlights that legacy core systems are a major obstacle to business efficiency: being complex, costly to maintain, and slow to adapt to change. As a result, banks often accumulate technical debt, a buildup of outdated systems and temporary fixes.

This leads to data silos, information trapped in separate systems, and makes integration expensive and slow.

Block #3: Depending too heavily on one tech provider, vendor lock-in, further limits flexibility.

Regulatory, security, and compliance challenges:

- regulatory compliance,

- auditability and accountability,

- security, privacy, and trust

Financial services are some of the most regulated industries in the world. Banks must prove that their systems are secure, auditable, and compliant with regulations like GDPR, PSD2, SOX, and Basel III.

As they adopt new tech, such as AI, open banking, and cloud, they must also ensure data privacy and cybersecurity, with an Ernst & Young survey revealing that 75% of global banking Chief Risk Officers view cyber risks as their top concern.

Keep in mind that a single breach could destroy customer trust and attract heavy fines 👇

For example, in 2023, Capital One paid $80 million in fines for compliance gaps following a data breach.

People, culture, and change management:

- resistance to change,

- cultural barriers,

- skills gap,

Digital transformation doesn’t just require new software; it demands a new mindset.

Employees must adapt to new workflows and learn new tools, but in traditional finance, change is often resisted, especially if people fear automation might replace their roles.

There’s also a skills gap, as modern finance requires expertise in AI, data analytics, and cybersecurity, not just accounting.

Maybe learning that 48% of digital initiatives meet or exceed their business outcome targets might help you take a step further 🤭

Finance digital transformation trends

Let’s check the trends of digital transformation in finance to better understand what it has brought to the industry so far:

1- AI-driven finance operations

Finance teams embed AI and generative models into their daily processes to speed up reporting, automate analysis, and enhance decision-making.

These tools learn from financial data in real time to forecast risks, detect fraud, and even create personalized offers for customers.

💡 According to this McKinsey report, AI adoption in finance could deliver $200–340 billion in annual value through automation and smarter decision-making.

Let’s take a look at how this trend plays out in different names in the industry:

- JPMorgan Chase uses a generative AI tool named IndexGPT to provide investment recommendations to clients, signaling a major shift toward AI-driven advisory.

- Mastercard integrates AI-powered anomaly detection to prevent fraud, improving detection rates by 20% to up to 300% in some instances.

2- Real-time finance operations

Traditional finance worked in monthly and quarterly reporting cycles.

Digital finance is now continuous, where data flows in real time, and transactions, reconciliations, and risk checks happen automatically without waiting for period closes.

Here are two good examples that highlight the outcomes of benefiting from real-time finance operations:

- This Deloitte case page shows how a company that moved from end-of-month closing to real-time dashboards and continuous accounting/real-time closing has helped them find opportunities for blockchain and robotic enhancements.

- SAP reports a 65% reduction in financial reporting time and a 50% reduction in financial analysis time after starting to use AI.

3- Open and embedded ecosystems

With digital transformation, banks are evolving into platform businesses, connecting financial services across industries via APIs.

Through embedded finance, consumers can access payments, loans, or insurance directly inside retail, travel, or e-commerce apps without visiting a bank’s website.

Let’s check two examples that have welcomed this trend:

- Starling Bank (UK) uses open APIs to let customers integrate accounting tools like Xero and QuickBooks, making cash flow tracking seamless.

- Apple Card is a perfect example of Banking-as-a-Service:

4- Secure, scalable, and human-centered finance

Nowadays, banks are rebuilding their digital infrastructure using modular components instead of one extensive system. This modular approach makes it easier to upgrade or replace specific functions like onboarding, lending, or compliance without disrupting the entire system.

At the same time, they’re strengthening zero-trust security, which verifies every user and connection to keep data safe.

To help employees and customers adapt to these new systems, digital adoption platforms (DAPs) guide users step by step, making complex financial tools easier to learn and use.

💡 Gartner predicts that 60% of banks will adopt modular or composable architecture to stay agile and secure.

Let’s move to the examples section, shall we? 👇

- Deutsche Bank and Google Cloud redesigned risk infrastructure using a composable approach, processing financial data 50% faster.

- UserGuiding enables financial solutions like Grupo IOB to onboard users faster, accelerating the adoption of new digital workflows.

How does UserGuiding help the finance digital transformation?

Financial institutions are introducing new digital tools faster than ever, but employees and customers often struggle to adapt.

In short, these systems never get adopted to the maximum extent, and digital transformation always gets delayed.

However, with a digital adoption platform that overlays directly on top of your existing software and guides users step-by-step in real time, employees and customers can learn by doing, instead of reading long manuals or attending repeated training sessions.

In the finance context, this helps institutions reduce onboarding friction, improve process accuracy, and accelerate the rollout of new tools across both staff and customer workflows.

Now, let me introduce you to the solution: UserGuiding, a digital adoption tool that enables banks and financial service providers to create interactive product walkthroughs, in-app guides, tooltips, and contextual help centers without writing code.

For example, it can help financial institutions:

- Onboard new employees faster: Instead of 1:1 training, new hires follow guided steps inside the banking software, reducing learning time and increasing confidence in handling processes like KYC checks, transaction approvals, and customer case management.

- Support change management when new systems are introduced: When a core system receives an update, guidance appears directly where users need to act, limiting mistakes and reducing resistance to change.

- Improve compliance consistency: By guiding users through required steps in AML, KYC, and audit workflows, UserGuiding helps teams follow internal policies correctly and reduces the risk of errors or skipped steps.

- Enhance customer-facing onboarding: Interactive walkthroughs inside digital banking platforms show customers how to transfer money, set up payments, or apply for services without calling customer support.

- Reduce support ticket volume: In-app resource centers allow users to solve their own questions instantly, decreasing reliance on help desks or call centers. Remember Grupo IOB’s story?

Take the GIF above as an example and imagine how useful it’d be in one of the scenarios above ☝️

Let me help you picture some of the benefits: For banks, the benefits include a faster onboarding for staff, smoother adoption of new tools, and lower operational strain on support teams; for customers, the outcome is a clearer, more intuitive digital banking experience.

Long story short, UserGuiding ensures that new technology in finance does not just get implemented, but actually gets used by placing guidance directly inside the applications people use every day.

.png)